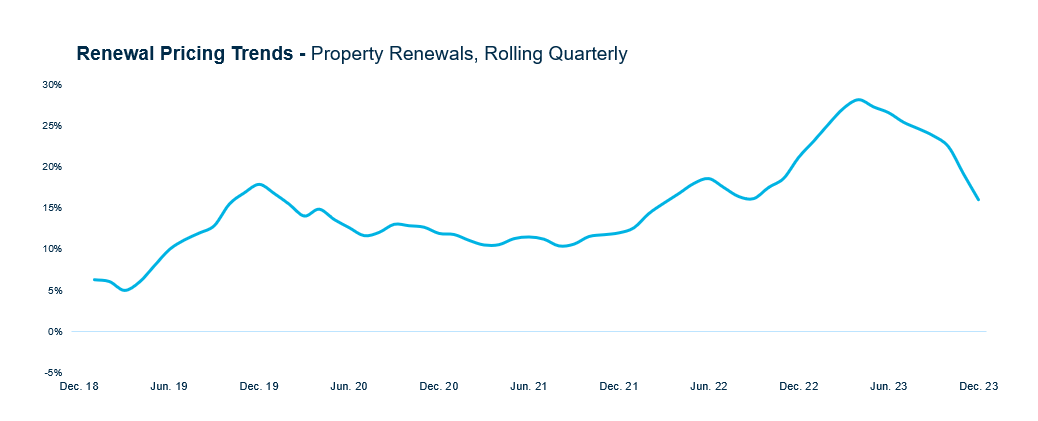

In our 2024 Property Outlook, we noted the property market was showing signs of softening and a slowdown in the pace of rate increases for most insureds was to be expected. As we move further into Q1, that prediction is ringing true.

Select image to view larger.

Of course, there are – and will continue to be – certain classes of business and geographic areas that will face higher rates as well as additional restrictive terms and conditions. CAT-exposed accounts will face ongoing challenges as carriers continue to manage their aggregate. And while we have seen some new markets enter, increased capacity is mostly due to carriers already in the market increasing line sizes and broadening their appetite.

The discipline in the market surrounding terms and conditions will most likely continue through 2024. Most carriers took larger retentions on their treaty placements forcing primary carriers to take on more risk. And with limited interest in frequency events, we expect deductibles to remain higher for the near future.

Reinsurance Renewal Season More Organized

This year’s reinsurance renewal season was much more organized, with only a few programs unable to purchase as much capacity as they wanted. Retention levels have stabilized, and rates stayed at or near where they ended in 2023. This was mainly due to:

There was a strong appetite for peak perils and higher excess layers with some programs signing back upper layers due to increased competitive capacity in the market. However, much of this “new” capacity was from current players in the reinsurance space. We expect capital markets will make additional capacity available if the market remains stable for an extended period of time.

Be on the Lookout:

A lot can change in a few months, especially given that most domestic markets will renew their treaties 4/1, 5/1 and 6/1. However, we remain confident that underwriting discipline and risk selection will prevail but that accounts with better risk characteristics (e.g., construction, losses, geographic location, industry class, etc.) will achieve better results when compared to 2023.

Market Trends to Watch in 2024

Despite 2023 being a relatively benign year, there are still headwinds in the market. For example:

- Severe Convective Storms (SCS) – The U.S. suffered losses of more than $50 billion from these storms alone in 2023. As a huge loss driver, much work has been done on deductibles and sublimits for this peril over the past few years. One thing that makes this peril especially difficult to rate for is the lack of historical data that has been collected.

- Wildfire – California suffered fewer wildfires and less total acreage burned in 2023 versus 2022. However, wildfire remains a difficult peril as the state’s proximate cause loss doctrine means it is basically impossible to exclude.

Changes to Moody’s RMS brings substantial updates to existing models and could still cause markets to be conservative with their CAT capacity. Version 23 addresses core perils and climate change views while introducing enhancements in geocoding, model flexibility, data framework and security. These alterations could ultimately result in unexpectedly high CAT losses in models and prompt carriers to shrink their capacity in markets already facing challenges. Given that many markets had only just begun to utilize RMS 23, we did not see any impact to midyear renewals. However as more markets adopt the latest version, it may drive probable maximum losses and deployment of aggregate in 2024. You can learn more about RMS version 23 here.

Conversely, when it comes to valuations, there is the potential for less scrutiny in 2024. Many accounts have worked diligently to ensure that their valuations have been updated and are more accurate based on current market conditions. Therefore, these valuations will not be decreasing, and many markets are still offering minimum acceptable ITVs.

Be on the Lookout:

In 2023, we saw 28 confirmed CAT events with losses exceeding $1 billion each. Only one of those events was a hurricane (Hurricane Idalia). This year’s season could change everything, so stay tuned.

Macroeconomics Remain a Concern

On December 13, 2023, the Federal Reserve held the Fed Funds Interest Rate at a target range between 5.25% to 5.5%. This, combined with a positive jobs report in January 2024, has led most experts to predict the Fed will begin to lower rates mid-year and increase predictions for an economic soft landing. However, turmoil in the banking sector continues to tighten access to credit as regional banks have outsized exposure to commercial real estate.

In Florida, a new law requiring condominiums to budget for both operating expenses and future repairs goes into effect January 1, 2025. With approximately 30% of condominiums fully-funded, many are still struggling – implementing new assessments to begin building that reserve now. This leaves little wiggle room to purchase full limits.

Be on the Lookout:

Floating rate loans that need to be refinanced over the next two years will likely be very painful for certain real estate owners experiencing higher interest rates at the time of refinance. This can instantly flip a property from being cash flow positive to cash flow negative, putting even more pressure on real estate owners to secure the most competitive insurance premiums they can find.

Partner With a Wholesale Broker

The market is changing fast, and we want to work with you to meet your clients’ evolving needs – ensuring your clients are taking advantage of the significant opportunities that brings. As carriers begin to re-evaluate attachments points, line size and rate increases, having a partner that understands their underwriting practices and appetite is priceless.

Amwins can be that partner. We place more than 65,000 property accounts through 300 markets each year, staying on top of property market conditions and industry trends to find solutions for your clients' most challenging risks. When you tap into our network of property specialists, you get 500 industry-fluent professionals who collaborate on risks to provide custom insurance solutions.

Contact your local Amwins broker today.