The U.S. solar market stands at around 85GW of installed capacity. This translates to about $120 billion in total insured values and $150 million in gross written premium (GWP) for property and casualty insurance. And the market is forecast to continue to grow rapidly with another 111GW to be installed by 2025.

The share of commercial and industrial-scale (C&I) solar construction activity is also set to expand. Historically, this segment was approximately 10% of all new solar construction in the U.S. However, over the next few years, this underserved market segment share is set to double.

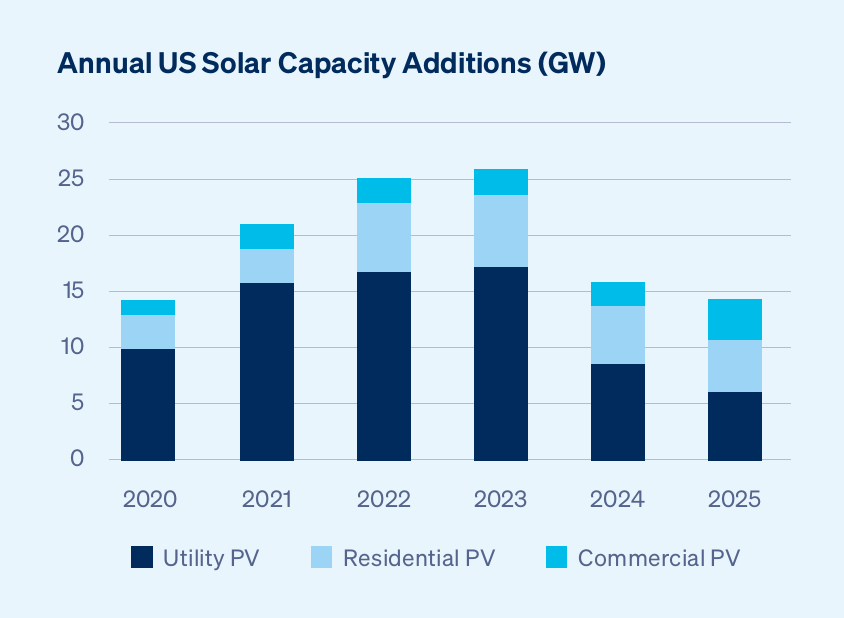

Chart source: EIA

One barrier to deployment is access to cost-effective insurance. For years, insurers have been attracted to the million-dollar premiums available on large, utility-scale solar projects. While insuring residential scale projects – think home rooftop solar – has been simple, through wrapping into general home insurance programs, it leaves a gap. C&I solar projects that are bigger than home solar but smaller than utility-scale – think solar farms connected to schools, hospitals, supermarkets and factories – have left brokers with slow service and expensive insurance.

C&I Solar: A Frustrating Market Segment for Insurance

For insurers, time not appetite is the problem. An underwriting review of a C&I solar project with an insured value of $2 to $20 million takes almost the same time as the review of a billion-dollar project. Mindful of opportunity cost, this means C&I solar reviews often end up at the bottom of the to-do-list.

To supply end-users, new utility-scale projects must be located near available slots on the electricity transmission grid. Typically found in California and Texas, these sunny locations and favorable power markets are limiting factors for siting a new project. And, since C&I project owners may fully consume the energy on-site, the potential number of grid slots and markets is bigger and the projects are more widely spread across the U.S. (It’s important to remember that if only part of the generated solar energy is transmitted to the grid, then a smaller slot is needed. Existing grid cables can only carry a limited amount of power before more or larger cables are needed.)

Another reason for the geographical spread of C&I is the commitment (or lack thereof) by public and private sectors to sustainability. In most cases, commercial entities that sell products and services to end-users are increasingly likely or have already committed to sourcing electricity from low carbon sources. Cheap solar panels and federal tax policies can also swing the economics enough to favor building your own supply of clean energy. (The barrier to making the economics of self-consumption with clean credentials work is separate from other challenges, including competing for the cheapest cost, seeking the same sunniest sites as utility-scale solar projects and finding the most favorable power markets for selling electricity.) Small values (those around $2 to $20 million per location), the associated smaller premium and disaggregated ownership means service from insurers for C&I solar is slow and insurance is expensive.

Ironically, insurers recognize this segment has a superior claims history with a lower natural catastrophe (natcat) profile than utility-scale solar. However, over the last five years, the frequency of secondary perils, particularly hail events, and the associated damage to utility-scale projects, have caused insurers to lower natcat limits and increase deductibles across all solar projects. As a result, inconsistent coverage year-over-year has threatened to derail new-build investment and compromise existing loan agreements.

For clients seeking to renew expiring terms, this has made purchasing natcat coverage for solar projects an expensive and protracted process, to the detriment of client service. Even worse, it often leaves clients to re-open loan agreements and re-negotiate minimum insurance requirements.

Finding a Quick, Cost-effective Solution

To address this inconsistency and support retail brokers looking to access the C&I market segment, Community Solar was conceived and developed by Nardac, in conjunction with best-in-class underwriters, modelers and claims handlers.

An instant quote-and-bind platform that bridges an attractive market segment for insurers with fast, cost-effective service for retailers, Community Solar delivers a seamless customer experience that enables brokers to obtain property quotes for operational C&I solar in just a few clicks. All policy documentation and invoicing are issued automatically.

Community Solar can also price and aggregate natcat coverage in real-time, producing instant, bindable quotes in minutes. It saves brokers time, negotiating terms and conditions and bringing certainty and quality coverage for their clients.

You can learn more about how Community Solar works both here and in this video. Or, if you are interested in binding coverage, you can contact Hannah Webb directly.