It’s only been six months since Hurricane Ian slammed into the coast of Florida as a Category 4 hurricane, wreaking havoc and leaving almost $50 billion in insured losses according to recent PCS estimates. The third most costly hurricane in U.S. history, Ian was recently upgraded by the National Hurricane Center (NHC) and listed as the fifth Category 5 hurricane to form in the Atlantic in the past five years.

The NHC has a new boss and from the looks of recent predictions for 2023, he has a busy season ahead of him. While this year’s hurricane season, which runs from June 1 through November 30, is predicted to be about average, Colorado State University is still expecting seven hurricanes – three of which will be major – and 15 named storms.

The 2023 report also includes the probability of major hurricanes making landfall, all of which indicates that despite there only being two such storms, there is a 44% chance they will impact the U.S. coastline and a 22% chance they will impact U.S. East Coast, including the Florida Peninsula.

As we kick off Hurricane Preparedness Week 2023, we examine the impact named storms have had on claims and why we can expect this high level of storm activity to continue.

Select image to view larger

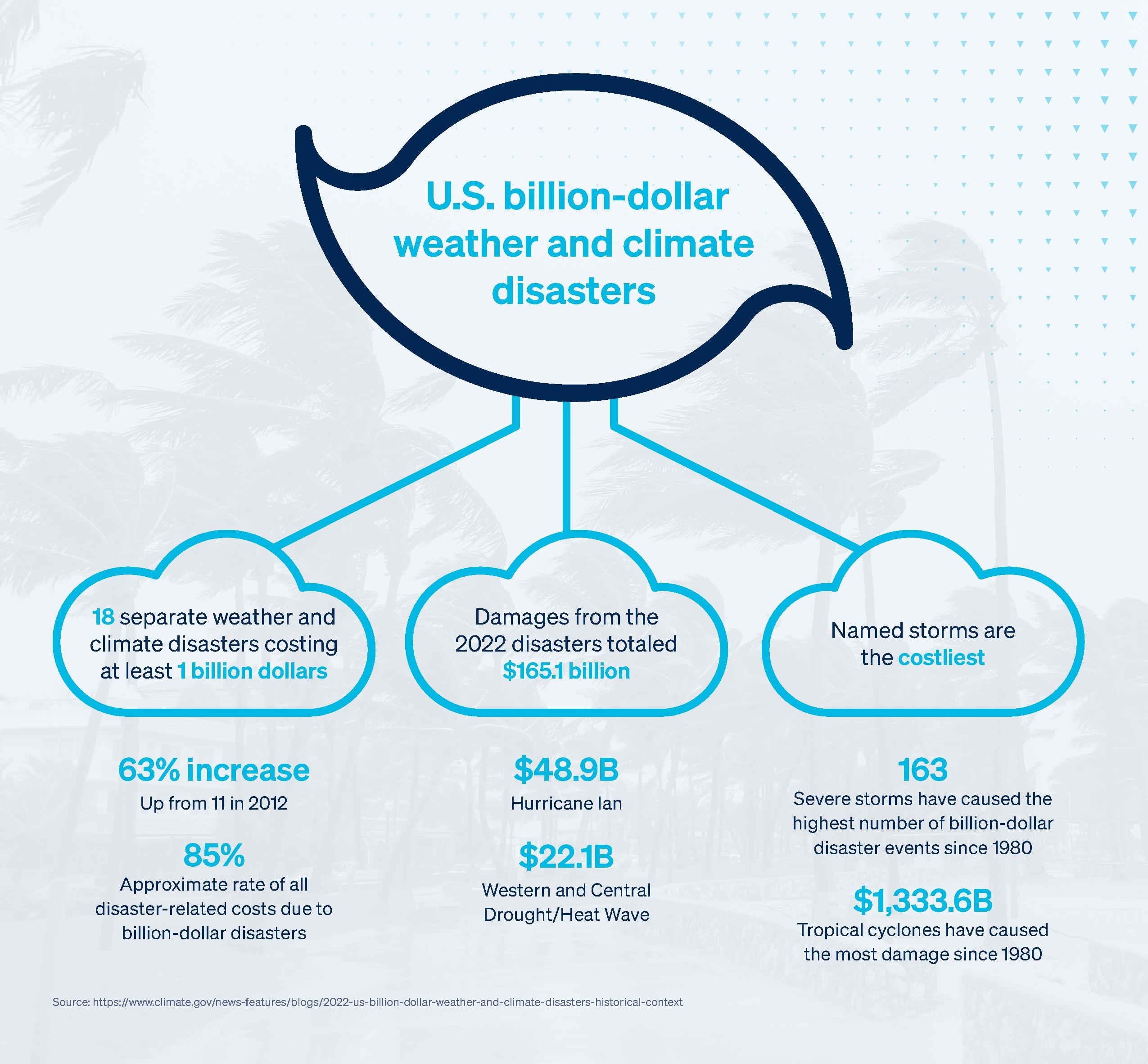

According to the National Centers for Environmental Information, there have been 348 weather and climate disasters with overall damages that exceeded $1 billion since 1980. In the last three years alone, 60 events have resulted in damages of more than $443 billion raising the question: Has this become the new normal, and if so, what’s behind the trend?

Top 3 factors impacting the increase in named storms and their resulting damage

1. Rising sea levels: According to the most recent report from NOAA and NASA, sea levels are rising much more quickly than experts predicted.

- Sea levels along the Gulf Coast and the southern Atlantic Coast have risen at an unprecedented rate, with an average increase of one centimeter per year since 2010.

- Sea levels along the U.S. coastline are projected to rise an average of 10-12 inches over the 30 years.

- Storm surge heights will increase and reach further inland by 2050, with moderate flooding expected to occur more than 10 times as often as it does today.

2. Climbing temperatures: Since 2012, global temperatures have increased by 0.22 degrees Fahrenheit.

- The world’s ocean surface temperature hit an all-time high in April 2023, leading experts to forecast a potential El Nino pattern in the tropical Pacific this year and resulting in a hurricane season that will be even harder to predict.

- Warmer oceans result in marine heatwaves around the globe and provide more energy for storms, intensifying certain weather events like hurricanes.

3. Increasing storm intensity:

- In 2022, the National Weather Service (NWS) provided storm summaries, a comprehensive review of significant storms, for 25 storms. This is a year-over-year increase of a 20% of large-scale storms and weather events.

- In the past five years, Hurricanes Harvey, Irma, Maria, Michael, Laura, Ida, and Ian – all Category 4 or 5 hurricanes – made landfall in the U.S.

In addition to climate-related factors, nearly 30% of the U.S. population now lives in population-dense coastal areas where building codes can be insufficient to reduce damage from extreme events and increases the likelihood of a catastrophic claim.

We help you win

In honor of National Hurricane Preparedness Week, April 30 – May 6, Amwins is here to help ensure that you and your clients are in the best position possible for safety and recovery should a hurricane strike.

Review our top 10 claims tips and checklist to help you prepare ahead of the 2023 storm season and to achieve fast, efficient handling of insurance claims afterward.

- If you have a claim to report as a result of a storm, the most efficient process is to report the claim directly to the carrier(s) in accordance with the reporting provisions of the policy. When submitting a claim, please include the insured's name and policy number.

Amwins believes that a strong defense is a good offense, and the time to help your clients understand their exposures is before they find themselves in the path of a natural disaster. We offer a wide range of services to aid you, from CAT modeling to claims advocacy, as well as parametric solutions and exclusive property capacity that continues to grow.

As always, we are committed to keeping you informed and armed with strategies for success. Reach out to your Amwins broker or underwriter for individualized attention.